Representative End User Clients

Representative Automation Clients

Representative Software Clients

To provide our Advisory Service clients with holistic coverage of the various industrial and automation markets we cover, ARC Advisory Group publishes indices of revenues from automation, and machinery companies as well as indices of revenues and CapEx from end-user industries on a quarterly basis.

This Special Report in PowerPoint format is concise and focuses more on the quantitative than the qualitative aspects of the automation, end-user, and machinery industrial markets.

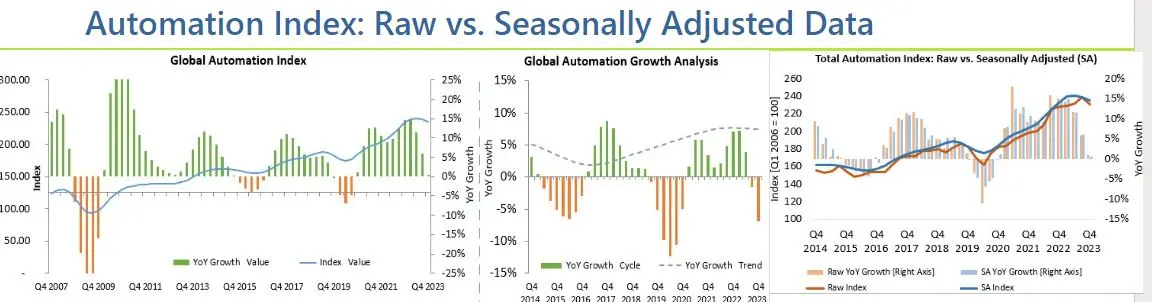

Global automation markets saw a marginal growth of just about 1 percent in Q4 2023 on YoY basis. The registered growth is the lowest growth figure since Q4 2020.

The growth cycle showed a marginal decline in Q3 2023 and shows further decline of about 7 percent per Q4 2023 results.

Demand from process and hybrid industry segments continued to remain strong, while the demand from discrete industry segments weakened due to normalization of backlogs, destocking, and declining orders on YoY basis.

Strong demand in oil & gas, refining, petrochemicals, data center, infrastructure, renewables, aerospace & defense, power generation and electrical distribution segments.

On seasonally adjusted basis, all the regions (Americas, Europe and Asia) saw marginal declines but at different levels, while the raw data shows that Americas was the only region, saw positive developments, Europe saw a marginal decline, and Asia was stable with no growth.

Demand for automation products continued to expand in the US market. The registered growth in Q4 2023 was low compared with Q4 2022 but it was almost at the same level compared with the YoY growth in Q3 2023.

Growth was predominantly driven by process, hybrid, and infrastructure industry sectors, notably energy transition, LNG, hydrogen, EV battery, and renewables.

Continued demand for process automation, systems, and electrical equipment (carbon capture, substation, power supply, and distribution).

Trends: sustainability, aerospace, defense, battery storage, EV, reshoring, supply chain diversification.

The YoY growth cycle pointed no growth in Q3 2023 and points to a marginal decline in Q4 2023.

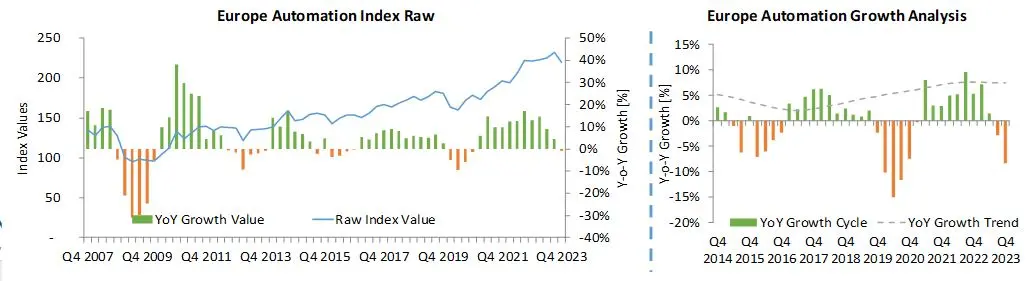

Automation markets in Europe saw a marginal decline for the first time since the market started to see a recovery from Q1 2021.

The YoY growth cycle pointed a decline of 3 percent in Q3 2023, and points further decline of about 8 percent per Q4 2023 results.

Slower demand for discrete automation segment and normalization of order patterns, decline in orders on YoY basis, destocking slowed down the growth both in revenues and orders.

While strong demand for process automation products, services, and systems from the process & hybrid industry sectors such as chemical, food & beverage, mining, energy, and oil & gas is expected to continue, demand from the discrete industries, including machine building, robotics, electronics, and semiconductors is expected to be weak for the next quarter and to see a recovery late this year.

Mega Trends: demand for automation, digitalization, electrification, hydrogen energy, decarbonization, and sustainability continue to pull the growth in Europe.

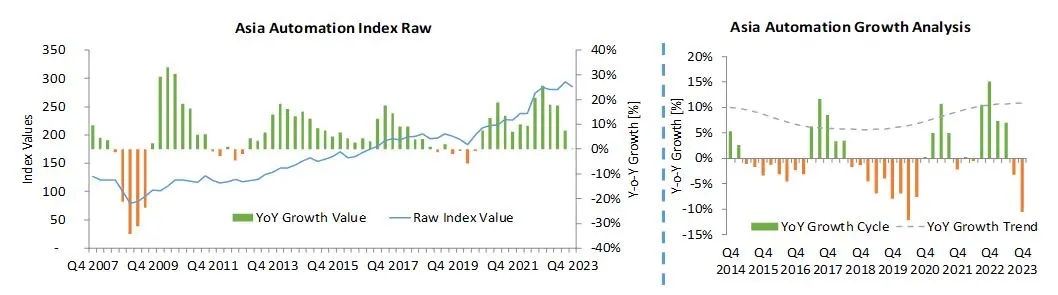

Since Q1 2022, the market saw double digit growth figures until Q2 2023, saw a lower growth of about 7 percent in Q3 2023, and the market was almost stable with no growth in Q4 2023.

The YoY growth cycle showed a decline of about 3 percent in Q3 2023 and shows a further decline of about 11 percent in Q4 2023, which is the highest decline in the last two years.

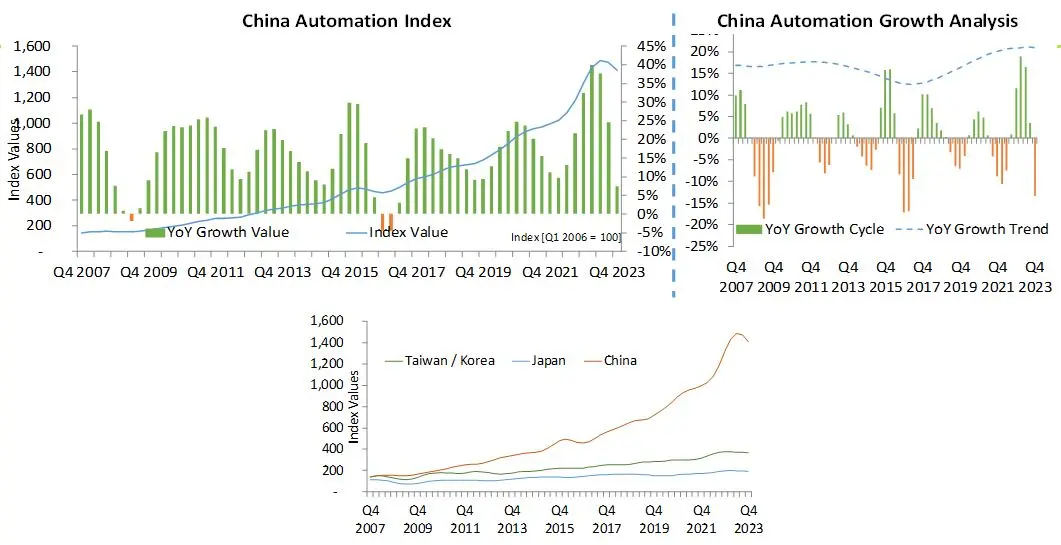

Continued slowdown in China’s manufacturing sector, strong demand from India notably in machine building, process industries, infrastructure, data centers, and renewables sectors.

In Japan, the economy continued to expand due to increase in consumer spending, strong demand in electric power generation, power supply and distribution and electrical equipment sectors.

Slower demand from semiconductor, and electronics machinery sectors. Investments related to transportation, infrastructure, electrification, renewables, digitalization, decarbonization, and circularity provide growth opportunities.

Automation Markets

Machinery Markets

End User Markets

Sentiment Index

ARC Advisory Group clients can view the complete report at the ARC Client Portal.

Please Contact Us if you would like to speak with the author.

Obtain more ARC In-depth Research at Market Analysis